October 2024

American Express — The Infuriating Credit Card

I've been an American Express customer since 2018, and recently I've realized how bad AMEX is in New Zealand when it comes to their product offering, customer service, and overall value proposition.

For a brand and card marketed towards wealthier card-holders, AMEX is downright the worst credit card I've held in New Zealand — even beats out the TSB Platinum card, which was decently bad.

Support call-centres in Australian timezone

Have a query around your credit limits, disputes, spend or something else? Don't bother calling before 11:30am NZDT, because the call centre is based in Sydney and doesn't start work until 8:30am their time. You may as well head into lunch before you can get anything sorted. What kind of service is this!?

Unilateral change to terms with no right to cancel

With most credit cards, the terms can be changed by the provider, but they'll generally allow you to cancel the card at any point with a pro-rated fee. With AMEX, not only do they change their earn rates and terms, but you have no ability to cancel the card for any sort of full or partial refund. So, if you recently signed up for the $1 APD for every $59 spend reward scheme for Airpoints Platinum, it's now changed to $70 spend, and you're stuck with it and the $195 in annual fees you've prepaid for the year.

Acceptance and higher surcharges

If you do all your shopping at big box retailers and live your life between Kmart, Bunnings, PakNSave, Woolworths, and the fuel stations, you'll be ok. But try and pay with AMEX almost anywhere else, and you'll just be holding up the queue and sounding like a douche bag with a card that isn't accepted. As a result, you'll end up carrying your AMEX and your debit card that's actually used most of the time.

When AMEX is accepted, many retailers add a higher fee to cover their own AMEX interchange fees — lovely!

Long bank transfer times

Suppose you want to pay down your card, or have spent to your limit and need to top-up again. With all other NZ credit cards at banks, you're able to directly transfer funds from your transaction account into your credit card account and have it processed immediately (e.g., ANZ) or same day (ASB). With AMEX, because they're not part of a bank, you have to wait up to 3 working days.

As a great example, I transferred funds Monday morning at 7:34am, and they did not appear until Tuesday night at 10pm. This is in the age of real-time, 7-day-a-week interchange functionality at all NZ banks. If you're travelling and accidentally hit your limit, best bet is you'll be credit-less for a few days.

Lack of Google Pay / Tech

Google Pay in 2024? Forget it.

Useless customer support

AMEX support is incredibly frustrating — there's no New Zealand presence at all; everything is done via Australia, Philippines, or India. They're very quick to pick up the phone or resume a live chat, but fairly useless at being able to advise or action anything. Here are some examples of interactions:

- Cancelling the card — Live Chat states it can be done within 30 days or 60 days pro-rata, but I must call. Calling AMEX, they advise that's not true. Goodbye.

- Overpaying the card — Read the saga below.

- Change of earn rate — Basically get told different dates and terms.

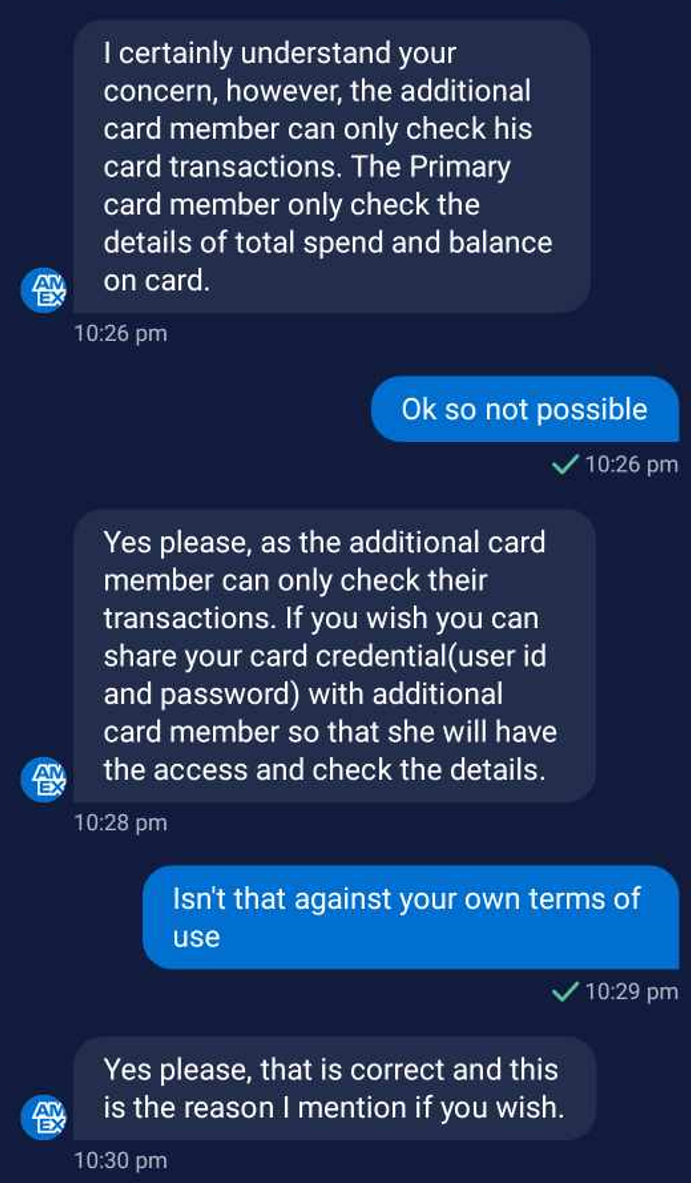

Blatantly encouraging sharing passwords

For all the world's cyber-security problems, hacks, and issues, nothing tops American Express support suggesting sharing a username and password with the supplementary card-holder to get around spend visibility issues — in violation of their own terms and conditions.

AMEX support's terrible advice on password sharing

Incredibly underweight travel insurance policy

The AMEX Airpoints Platinum card offers domestic and international travel insurance (one that's advertised frequently), but digging into the details reveals it's incredibly underpowered and won't actually be much help when you need it most.

Let's compare it to the ANZ Airpoints Platinum card — comparable and even cheaper in annual fees — using some common scenarios:

Lost passport

AMEX only provides $500 cover with a $100 excess, so $400 net to help you get a new passport. It also only covers replacement costs and emergency travel documents. ANZ meanwhile offers $5,000 with a $200 excess ($4,800 net), and includes cover for additional accommodation and transportation expenses (suppose you need to stay in a city a few extra days or run to the capital to the embassy).

Getting sick for a few days

Both offer medical coverage (though AMEX is a stingy $1,500 unapproved), but there is only $250 per claim in reimbursement for cancelled activities, whereas ANZ offers unlimited coverage for resumption of journey. Crazy! Icing on the cake is the $250 excess AMEX charges.

Delayed connecting flight

ANZ offers up to $15,000 including accommodation, meals, and other reasonable expenses. AMEX? $500 for a delay maximum, and a $100 excess. Worse still, you need to pay for everything on the AMEX — good luck with their overall acceptance.

Reading the policy wording, it goes on — basically the AMEX card pretends to offer travel insurance, but in most cases, you're getting nothing in the event of an actual claim situation.

Very strict travel insurance activation terms

This one broke the straw on the camel's back for me — American Express has incredibly strict eligibility criteria for their travel insurance activation. The key one being:

You pay the full amount of your return ticket for a Scheduled Flight or Scheduled Cruise leaving New Zealand on your American Express Card Account and/or Air NZ Airpoints. If the airline does not accept American Express or has higher fees, you will not be able to activate travel insurance — no further appeal.

What caught me out was the strictness of "full amount" or "full fare" — I paid for $5,000 worth of Qantas flights with the American Express and burnt $20 of Points + Pay. Because this was not considered the full amount, my travel insurance was void.

No insurance for supplementary card-holders

With most bank platinum cards, your additional card-holders are eligible for the same insurance policies you are — so your spouse can book and travel and leverage the travel insurance policies. American Express does not offer that; they must be booked on your card and be travelling with you at all times for the insurance to be offered (not that the insurance policy offers much).

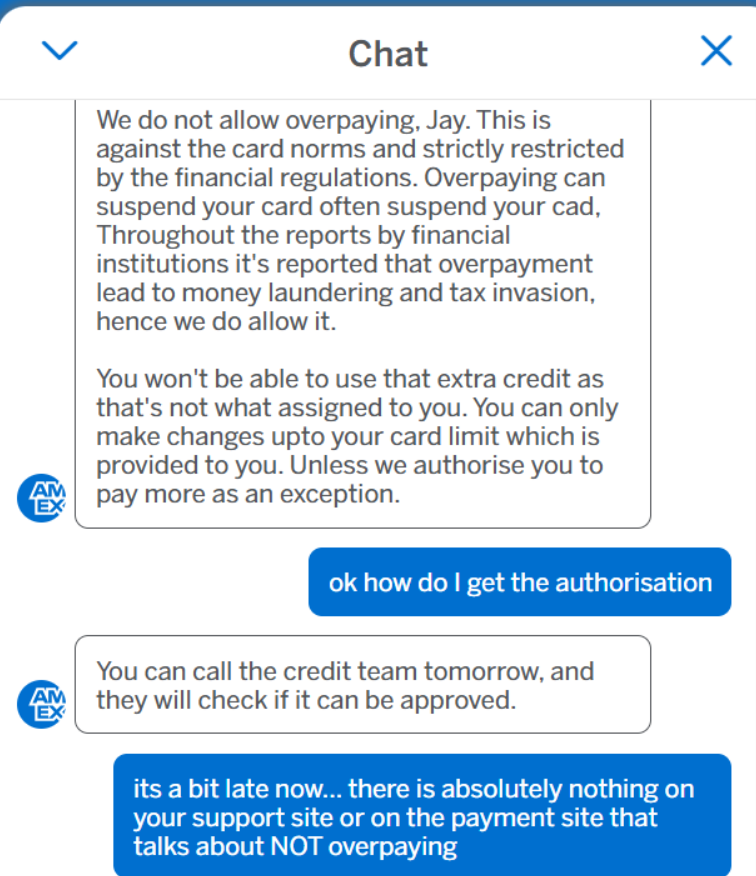

Card suspension for pre-loading / overpaying balance

As is often the case when booking travel for multiple people, the amount being spent goes over the assigned credit limit. With most credit cards, you can load extra funds on to it temporarily and spend it on the travel you were planning — no issues.

With American Express, not only is it not allowed, they don't tell you anywhere you can't do so. Trying to clarify it with their support team gets you a passive-aggressive (or maybe just straight aggressive) threat to suspend your card and accusations of money laundering and tax "invasion," with a caveat that they allow it (just bad English, also an issue).

When I called their customer support (based in AU), I got a bloke threatening me with a card suspension until the funds were returned, bristling that I had dared move $5K pre-emptively to my AMEX to pay for travel.

To add insult to injury, there is absolutely nothing in their FAQs, and nothing anywhere else that says you can't do it, and there's no sort of payment block.

The response regarding card suspension for overpaying

Priority Pass — main cardholder only

Minor one but annoying nonetheless, the Priority Pass program is only offered to the main cardholder; the supplementary is treated as a guest and must pay for entry. Reading the T&Cs, this isn't mentioned, as it refers to "cardholders" generically.